Kemi Badenoch’s bold proposal to scrap Stamp Duty on mainresidences has sent ripples through the industry. And now, all eyes are on Chancellor Rachel Reeves to see if she’ll follow suit.

Because while Stamp Duty might be one of the most unpopular parts of buying a home, it also brings in around £9 billion a year. So if it goes, what replaces it? And how will that affect the market?

What’s at Stake

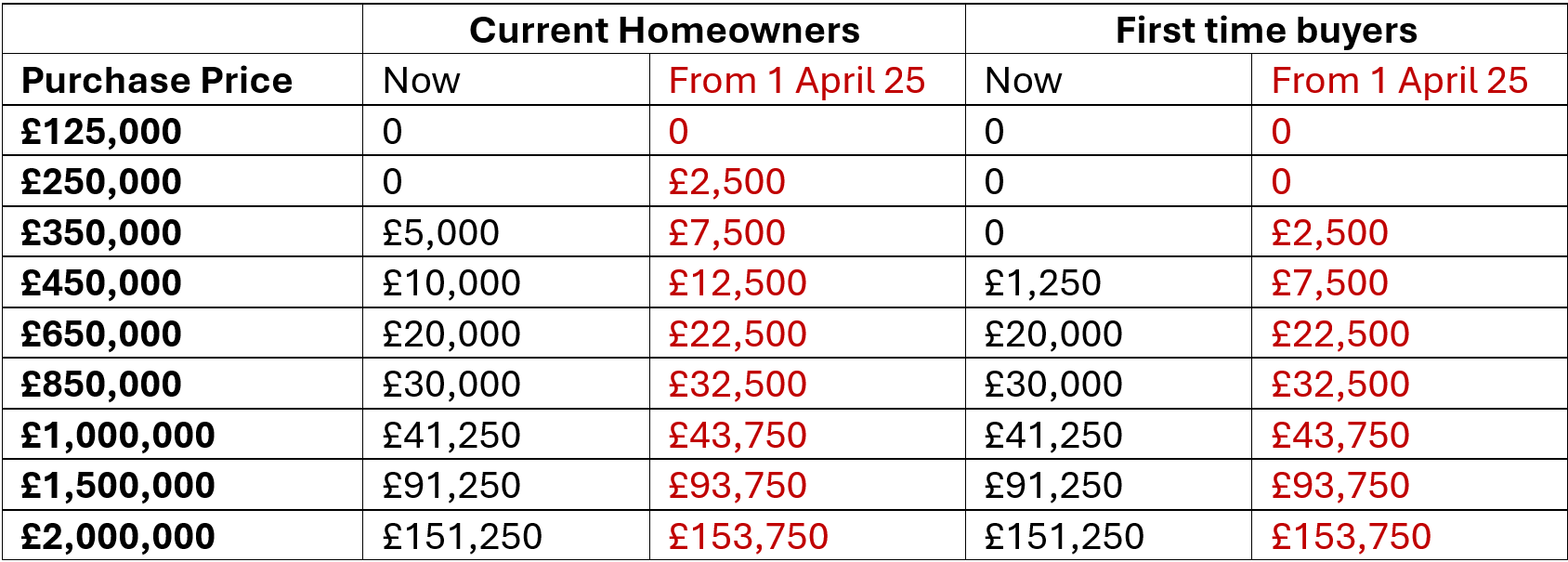

Stamp Duty Land Tax (SDLT) has long been a financial hurdle for buyers in England and Northern Ireland. It’s one of those hidden costs thatquietly shapes the housing landscape, influencing when people move, how muchthey spend, and even where they live.

Abolishing it could transform that landscape. But it could also reshape government finances and housing affordability in unexpected ways.

The Upside

A Boost in Market Activity

Removing Stamp Duty could encourage more people to buy,sell, and move. That means more transactions, more listings, and a healthier market flow, good news for buyers, sellers, and agents alike.

Relief for First-Time Buyers (Where It Counts)

Let’s be clear: first-time buyers already benefit fromStamp Duty relief they pay nothing on homes up to £425,000 and reducedrates up to £625,000. But in high-value areas like London and the South East,plenty of entry-level properties still sit above those thresholds.

So while it won’t help every first-time buyer, removing Stamp Duty completely could ease pressure in overheated markets, whereeven getting on the ladder is a stretch.

Better Mobility

Many homeowners stay put longer than they’d like because of Stamp Duty costs. Scrapping it could help people move more freely whether todownsize, relocate for work, or move into a home that actually suits theirlifestyle.

The Flip Side

The £9 Billion Question

Stamp Duty brings in around £9 billion a year. If itdisappears, the government has to make that up somewhere, and that likely means higher taxes elsewhere or cuts to public services.

But instead of shifting the burden, could this be anopportunity to create something better?

A Better Approach: Reform That Supports the Market, NotJust the Treasury

Rather than replacing Stamp Duty with another catch-all tax like a land value tax which still burdens owners, this could be a chance to rethink the system in a way that helps people move more easily, fairly, andefficiently.

Here’s what that could look like:

A Regionally Adjusted System

Not all areas are created equal and neither are their property values. A £500,000 home in London is considered fairly standard, while in parts of the North it’s a high-end purchase. Instead of national thresholds, Stamp Duty bands could beadjusted by region, so buyers aren't penalised simply for living inhigh-cost areas.

Phased or Deferred Payment Options

Stamp Duty is often the deal-breaker at the point ofpurchase. With deposits, legal fees, and moving costs piling up, it's one moreupfront burden that stops people from moving.

Allowing buyers to pay Stamp Duty in instalments or deferit (until they sell the property or after a fixed period) could relievethat pressure without removing the revenue entirely.

Incentives That Unlock Housing Stock

One of the biggest challenges in the UK is housing that’snot being used efficiently particularly under-occupied family homes.

By offering Stamp Duty discounts to downsizers, wecould encourage older homeowners to move into more suitable homes freeing uplarger properties for families who really need the space.

What This Means from Different Perspectives

From a Landlord’s Point of View

Stamp Duty reform won’t directly benefit landlords, sincebuy-to-let purchases are taxed differently and likely will continue to be.But if the government decides to recover lost revenue through higher CapitalGains Tax or reduced reliefs, landlords could take the hit indirectly. Thatmight reduce investment in the sector, and in turn, limit rental supply.

From an Investor’s Point of View

If Stamp Duty is removed for residential buyers, competitionfor properties could rise, especially in high-demand areas. But if newtaxes target investment properties to make up the difference, returns could besqueezed. That could lead investors to rethink their strategy, particularlythose holding large portfolios.

From a Tenant’s Point of View

Tenants don’t pay Stamp Duty, but they may still feel theimpact. If landlords leave the market due to new taxes or reduced profits,rental supply could shrink pushing rents up. On the other hand, if reformslead to more available housing overall, tenants might benefit from betteroptions and, eventually, improved affordability.

Remove or Reform?

There’s no denying that Stamp Duty is outdated andunpopular. It discourages movement, adds cost and complexity, and blocks peoplefrom buying or selling when they need to.

But abolishing it entirely without a well-thought-outreplacement risks creating bigger problems.

This could be an opportunity to do something smarter. Notjust to move money around, but to create a system that actually works:

The Real Conversation

At KAPS, we see both sides of the equation, buyers,landlords, investors, and tenants, all navigating the realities of today’sproperty landscape.

Stamp Duty reform could reshape the playing field. Butwhether it levels it or tilts it further, depends on how it’s handled.

What’s your view?

Would removing Stamp Duty truly open doors for more buyers,or simply shift the cost somewhere else?

And if it goes what’s the fairest way to replace it?

Join the conversation with us we’d love to hear yourtake.

Guaranteed Peace of Mind from One Landlord to Another

.svg)

.svg)

.png)